Political Suasion

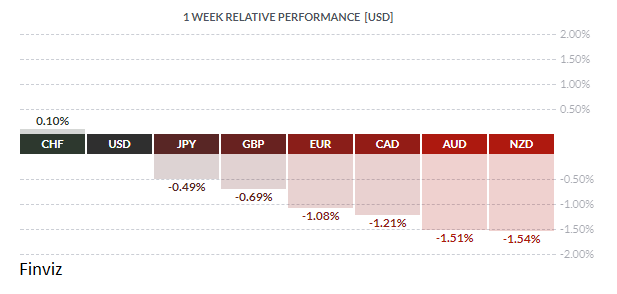

It was bound to happen at some point. After what seemed an interminable period of USD weakness, the greenback finally showed some signs of life. At the same time, a number of political developments in America and elsewhere caused investors to re-assess their outlook on currencies and rates. We’ll take a brief look at these, starting with the recent federal elections in Eurozone stalwart Germany.

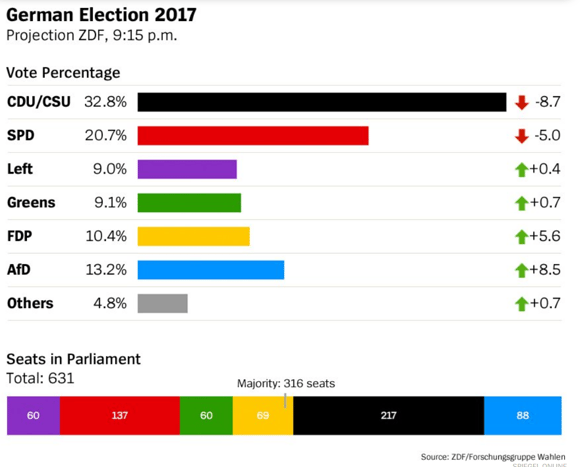

As was widely expected, Chancellor Angela Merkel was elected to a fourth term. However, the win came at a high price, with defections of many supporters from Frau Merkel’s Christian Democratic Union (and its Bavarian sister party Christian Social Union) leading to a fall in their joint support by almost 9% to a post-1949 low. Much of this support, at first glance, appears to have switched to the populist Alternative for Germany (AfD). The surprise results for the AfD – now the third-largest party in the Reichstag – indicates that the voter revolt first seen last year in Brexit and the subsequent election of Donald Trump may still be ongoing.

Bundeskanzlerin Merkel has apparently received a sharp rebuke from the voters and, given she may have to compromise to a considerable degree in any coalition to maintain her hold on power, the strong leftist tilt of her government may be softened. Unsurprisingly, she and her party were subdued as the results came in. Additionally, as zone paymaster, Germany may not be as willing as before to be the financial foundation of the entire Eurozone project. Obviously, effects on the EUR will play out over time, but a seismic shift may have occurred here.

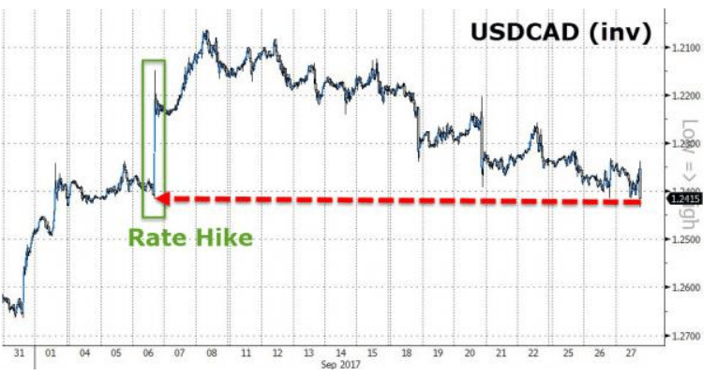

In the True North, Bank of Canada Governor Stephen Poloz apparently poured cold water on any thoughts of aggressive rate hikes in the near-term, in remarks made in a speech last Wednesday. In his speech, Mr. Poloz said that there is no ‘predetermined path for interest rates’ and, as a result, the Bank would proceed ‘cautiously’. Some other remarks:

'The appropriate path for interest rates in this situation is very difficult to know, because there are a number of unknowns around the inflation outlook'

'We will not be mechanical in our approach to monetary policy.'

Mr. Market had no difficulty interpreting these remarks, pounding the loonie mechanically and taking it back to levels where it traded prior to the Bank’s most recent hike in the overnight rate.

Courtesy Zero Hedge

Back to earth (Inverted RH column)

On the other hand, our learned colleagues Dr. Long and Mr. Short dissected Mr. Poloz’s speech and jointly feel that, while the governor would like to normalise interest rates, still he is wary of stifling a fledgling recovery. His task is to steer a middle path between raising rates while letting the economy grow, remaining cognizant of the fact that most Canadians are over-indebted and, basically, tapped out. (Not So Fast – September 11, 2017)

JPY was relatively quiet on the week, despite political manoeuvring by the governing Liberal Democratic Party. Prime Minister Shinzo Abe called a snap election ostensibly to deal with the ‘national crisis’ but in reality to take advantage of favourable polling numbers and disarray in the main opposition Democratic Party. The ‘national crisis’ is a red herring; Japan has been in economic crisis since 1990 and an end anytime soon is, frankly, doubtful. Rather, PM Abe has been gaining support for his forceful dealing with rogue North Korean leader Kim Jong-un. However, both Angela Merkel and British PM Theresa May could advise Mr. Abe of the risks of snap elections in today’s unsettled times.

So what happened in the land of the free? Middling economic statistics, Fedspeak and politics, that’s what. On balance, the week’s array of secondary stats were alright, but only that. Anyone looking for evidence of strong economic growth would have to look elsewhere. The one bright spot, however, was Q2 GDP, revised from the initial +3.0% to +3.1% - a pleasant upward tick. A number of Fed speakers held forth on the economy but said little of note; on the other hand Fed Chair Janet Yellen made clear her wish to continue raising the Fed Funds rate despite her puzzlement with continuing low levels of price inflation.

The major issue was last Wednesday’s unveiling of tax reform proposals by President Donald Trump and the GOP to almost universal derision by Democrats and others. The latter was expected, hence unsurprising. Once again our colleagues Dr. Long and Mr. Short analysed the proposals and summed them up as follows:

- Tax relief for middle-class families.

- The simplicity of "postcard" tax filing for the vast majority of Americans.

- Tax relief for businesses, especially small businesses.

- Ending incentives to ship jobs, capital, and tax revenue overseas.

- Broadening the tax base and providing greater fairness for all Americans by closing special interest tax breaks and loopholes.

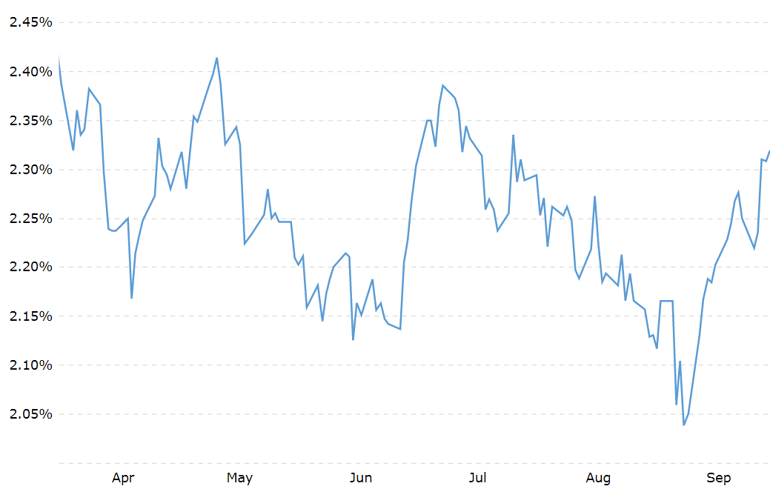

Which brings us to the treasury market. We had a chat with our friend the bond salesman about reaction in the fixed income market to all these developments. He told us that dismay would be an appropriate term, with bond traders – always a fearful lot – fretting over the Fed’s apparent determination to raise rates and reduce its balance sheet, while potentially stronger economic growth threatened rising inflation. Additionally, the salesman continued, Mr. Trump’s tax proposals might threaten ballooning federal deficits going forward and an avalanche of new treasury supply. With the Fed no longer buying treasurys, he added, yields have nowhere to go but up, taking administered rates along with them

Courtesy Zero Hedge

10 year US Treasury Yield – The global benchmark bond takes a hit!

The coming week sees quite a few notable statistics, chiefly US and Canadian employment numbers due out this Friday.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, OCTOBER 2 | ||||

| 04:30 | GBP | Manufacturing PMI | 56.3 | 56.7 |

| 10:00 | USD | ISM Manufacturing PMI | 57.9 | 58.8 |

| 23:30 | AUD | Cash Rate | 1.50% | 1.50% |

| 23:30 | AUD | RBA Rate Statement | ||

| TUESDAY, OCTOBER 3 | ||||

| 04:30 | GBP | Construction PMI | 51.2 | 51.1 |

| WEDNESDAY, OCTOBER 4 | ||||

| 04:30 | GBP | Services PMI | 53.3 | 53.2 |

| 08:15 | USD | ADP Non-Farm Employment Change | 151K | 237K |

| 10:00 | USD | ISM Non-Manufacturing PMI | 55.5 | 55.3 |

| 10:30 | USD | Crude Oil Inventories | -1.8M | |

| 13:15 | EUR | ECB President Draghi Speaks | ||

| 15:15 | USD | Fed Chair Yellen Speaks | ||

| 20:30 | AUD | Retail Sales m/m | 0.3% | 0.0% |

| 20:30 | AUD | Trade Balance | 0.87B | 0.46B |

| THURSDAY, OCTOBER 5 | ||||

| 08:30 | CAD | Trade Balance | -3.0B | |

| 08:30 | USD | Unemployment Claims | 270K | 272K |

| FRIDAY, OCTOBER 6 | ||||

| 08:30 | CAD | Employment Change | 22.2K | |

| 08:30 | CAD | Unemployment Rate | 6.2% | |

| 08:30 | USD | Average Hourly Earnings m/m | 0.3% | 0.1% |

| 08:30 | USD | Non-Farm Employment Change | 88K | 156K |

| 08:30 | USD | Unemployment Rate | 4.4% | 4.4% |

|

by DAVID B. GRANNER Senior FX Dealer, Global Treasury Solutions |