Winds from Wyoming

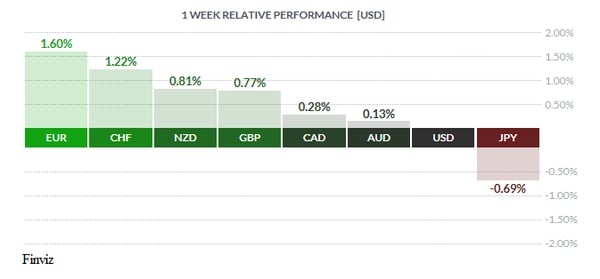

You wouldn’t know it from last week’s relative performance chart but the Australian dollar was the most volatile currency of the lot. The AUD fell over a cent on Thursday and then recovered by three quarters of cent on Friday as the 24 hour political turmoil was resolved, for now. In the end, Scott Morrison unseated Malcolm Turnbull in a party rebellion to become Australia’s prime minister, marking a rightward shift for the ruling coalition as it grapples with the rise of fringe parties akin to those that have realigned politics in the US and Europe. This was the sixth time Australia has switched prime ministers in about a decade as no leader has been able to survive a full term without being ousted by their own party. Interestingly, the US isn’t the only country with trade tensions with China – Australia is as well. Earlier in the week, Australia banned Chinese telecom firms Huawei Technologies Co. and ZTE Corp. from its next-generation 5G mobile network, due to concerns about the possibility of cyber spying by China. Looks like trade tensions are contagious or are they coordinated?

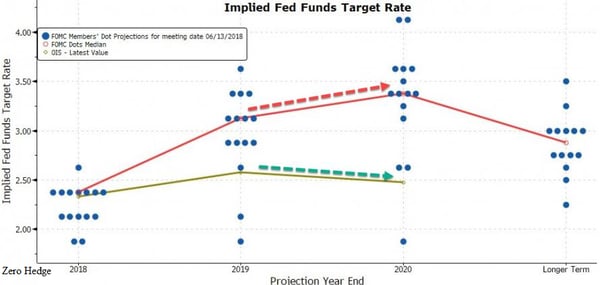

Moving to another political hot potato – central bank independence from political interference. President Trump was at it again last week as newswires reported that he complained about the Federal Reserve’s rate hikes at a Hampton’s fundraiser. We shouldn’t be surprised; this is the second time in less than 30 days that he’s made comments about his displeasure over Fed rate hikes. Central bank independence is supposed to be sacrosanct and not to be interfered with or the next thing you know your currency is in a free fall. A recent example of this has occurred in Turkey where President Recep Tayyip Erdogan has repeatedly pressured the country's central bank to cut interest rates. Personally, I don’t think that President Trump thinks he can influence the Fed, I think he is thinking ahead and setting up the Fed to take the blame for the next recession. Having said that, if the Fed raises interest rates in September but fails to raise rates again in December, then the perception will be that the Fed succumbed to the President’s pressure, regardless of whether it’s true or not. Sure enough, it looks like this week’s central bank shindig at Jackson Hole, Wyoming provided this situation.

The Jackson Hole Economic Symposium is an annual symposium, sponsored by the Federal Reserve Bank of Kansas City since 1978, and held in Jackson Hole, Wyoming, since 1981. The symposium focuses on an important economic issue that faces US and world economies. With the head of the European Central Bank and the Bank of Japan deciding not to attend this year, the spotlight would clearly be on the new Chairman of the Federal Reserve, Jerome Powell with his speech on “monetary policy in a changing economy”. Everyone knows, including the central bankers themselves that every word spoken will be scrutinized for every minute detail. With this in mind, we should take very seriously the reaction of Mr. Market to the speech made on Friday by Powell.

Prior to Powell’s speech, the Fed was on a clear path for the next year or so. It was going to raise rates again, in September and December, raise rates a few more times next year, and continue with its balance sheet roll off. As Powell spoke, US equities rose to a new all-time intraday record, the yield curve flattened, and the USD fell against most of its peers. It seems that Mr. Market had a dovish take on the speech and choose to focus on the following comments – “We have seen no clear sign of an acceleration above 2%” in inflation, he said, and “there does not seem to be an elevated risk of overheating”. Also, Powell deliberately said he was avoiding all foreign and political questions, admitting that these were risk factors that “could demand a different policy response, but today I will step back from them”. These comments failed to deliver a clear signal that the Fed needed to keep tightening. Furthermore, his predictions for future tightening were strictly conditional - “If the strong growth in income and jobs continues, further gradual increases will likely be appropriate.” The speech has cast doubt on a December rate hike and puts the chance of even one more hike next year at only 60%.

It seems the winds off the Wyoming plains have the capacity to give Mr. Market the chills.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, AUGUST 27 | ||||

| TUESDAY, AUGUST 28 | ||||

| WEDNESDAY, AUGUST 29 | ||||

| 08:30 | USD | Prelim GDP q/q | 4.0% | 4.1% |

| 10:30 | USD | Crude Oil Inventories | -5.8M | |

| 21:00 | NZD | ANZ Business Confidence | -44.9 | |

| 21:30 | AUD | Private Capital Expenditure q/q | 0.6% |

0.4% |

| THURSDAY, AUGUST 30 | ||||

| 08:30 | CAD | GDP m/m | 0.5% | |

| FRIDAY, AUGUST 31 | ||||

|

by TONY VALENTE Senior FX Dealer, Global Treasury Solutions |