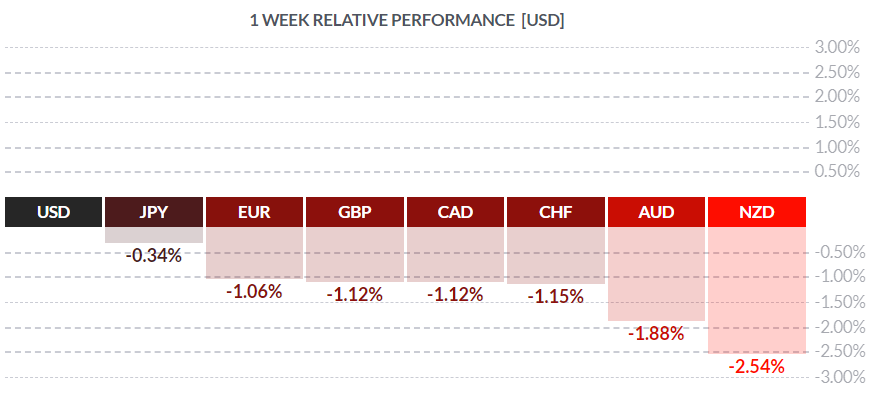

Courtesy FinViz

This past week saw a major rebound in the USD following marked greenback weakness in the week prior. Last week our colleague laid out the technical case for USD bearishness (“Mexican Stand-off”). Now, with the assistance of our learned colleagues Dr. Long and Mr. Short, we will examine the fundamental case for USD bullishness.

To our Canadian readers – sadly, there were no statistics of note released in the True North last week. However, it was remarked that the astonishing indebtedness of Canadians, at $2.230 trillion CAD, now exceeds the size of the total domestic economy at $1.900 trillion CAD. This issue has been well-documented in prior dispatches, so we won’t re-hash it here. Still, it’s remarkable how large this amount is and how it continues to grow apparently unchecked. Last month saw an increase of $20 billion CAD, 65% of it in new mortgage debt. Given that the domestic economy is underperforming on all fronts, save employment (and some are becoming sceptical of these numbers), we doubt this will end well.

At the beginning of last week, the greenback was unloved; however, a combination of good economic statistics and an unsettled international situation (now there’s a surprise!), along with a profit-taking bounce, saw the USD beat all comers. Let’s take a closer look...

Both US May PPI and CPI inflation numbers were released last week, showing continued moderate price inflation of around +0.2% mth/mth. These were non-events for traders more concerned with the reception being accorded a heavy treasury auction calendar. Last Tuesday, Wednesday, and Thursday saw 3-year, 10-year, and 30-year bond auctions and (as our colleague pointed out last week) there was major concern about a potential lack of buyers. In any event, all three auctions went extremely well, the treasury obtaining its needed cash at reasonable rates, bond traders breathing a huge sigh of relief, and the bond market rallying in response. This provided major support to the USD. Then, last Friday saw the release of numbers that appeared to dispel the recent view that the US economy was fading rapidly, and that the Fed would be cutting rates aggressively over the next 18 months. May Retail Sales at +0.5% slightly missed the call of +0.6%, but April was revised upwards to +0.3% from the previous -0.2%, a strong revision. Perhaps May will be revised upwards in the next report?

May Industrial Production was also released last Friday, rising a smart +0.4% vs the call of +0.2% and showing the largest mth/mth increase since November of 2018. May Capacity Utilisation also rose to 78.1%, well above the previous 77.9% and beating the consensus call of 78.0%.

These results support the greenback and, at least for now, call into question this whole rate-cut scenario. The Fed is scheduled to make a rate announcement this week following their two-day meeting June 18-19, and it shall be quite interesting to hear what they have to say.

We have also mentioned the unsettled international situation; unsurprisingly, it involves Iran and oil. Two tankers were attacked in the Strait of Hormuz, both ships either under Japanese ownership or hire, but neither sank and all hands were rescued. The incident occurred at the same time Japanese PM Shinzo Abe was in Tehran speaking with Iran’s leadership, causing some analysts to believe it was unlikely the Iranians were behind this attack.

Initially the crude market rallied about 2% or so, giving back its gains as more information became available. Still, there is considerable confusion and speculation as to the cause and the culprit of the attack. Regardless, US Secretary of Defense Mike Pompeo fingered Iran as the miscreant, sufficient to ratchet up tensions another notch between the two adversaries and providing a safe-haven bid to the USD. Bottom line: With a steady economy, a calmed-down treasury market and now with rising international tensions, the greenback may be set for further near-term gains. Mr. Market will listen very carefully to the Fed on Wednesday.

Elsewhere, in Europe and the Far East there was nothing to report.

This week sees the previously-mentioned two-day FOMC meeting – likely to dominate market action - along with a mix of secondary statistics from both sides of the border.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, JUNE 17 | ||||

| 13:00 | EUR | ECB President Draghi Speaks | ||

| 21:30 | AUD | Monetary Policy Meeting Minutes | ||

| TUESDAY, JUNE 18 | ||||

| 04:00 | EUR | ECB President Draghi Speaks | ||

| 00:30 | AUD | RBA Rate Statement | ||

| WEDNESDAY, JUNE 19 | ||||

| 04:30 | GBP | CPI y/y | 2.0% | 2.1% |

| 08:30 | CAD | CPI m/m | 0.1% | 0.4% |

| 10:00 | EUR | ECB President Draghi Speaks | ||

| 14:00 | USD | FOMC Economic Projections | ||

| 14:00 | USD | FOMC Statement | ||

| 14:00 | USD | Federal Funds Rate | <2.50% | <2.50% |

| 14:30 | USD | FOMC Press Conference | ||

| 18:45 | NZD | GDP q/q | 0.6% | |

| 22:35 | AUD | RBA Gov Lowe Speaks | ||

| Tentative | JPY | Monetary Policy Statement | ||

| THURSDAY, JUNE 20 | ||||

| Tentative | JPY | BOJ Press Conference | ||

| 04:30 | GBP | Retail Sales m/m | -0.5% | 0.0% |

| 07:00 | GBP | MPC Official Bank Rate Votes | 0-0-9 | |

| 07:00 | GBP | Monteary Policy Summary | ||

| 07:00 | GBP | Official Bank Rate | 0.75% | 0.75% |

| 16:00 | GBP | BOE Gov Carney Speaks | ||

| FRIDAY, JUNE 21 | ||||

| 03:15 | EUR | French Flash Services PMI | 51.6 | 51.5 |

| 03:30 | EUR | German Flash Manufacturing PMI | 44.6 | 44.3 |

| 03:30 | EUR | German Flash Services PMI | 55.3 | 55.4 |

| 08:30 | CAD | Core Retail Sales m/m | 0.6% | 1.7% |

|

by DAVID B. GRANNER Senior FX Dealer, Global Treasury Solutions |

|||