Here we go again! Game on: the race to the bottom has restarted. This past week, we learned that the major central banks of the world are hell bent on extending a business cycle that is very long in the tooth. Of course, they can afford to do this because (according to their statistics) inflation is low and below their 2% inflation targets. Don’t even get me started on this one! For the life of me, I can’t understand why anyone would want an annual inflation rate of 2%. A 2% annual inflation rate means that prices double about every 9 years. Why exactly would I want this? While we’re on the subject, the other side of the coin drives me to equal madness; when politicians say that their domestic currency is too strong. Wait a second… as a citizen and a consumer, I don’t want a weaker currency. I don’t want to spend more to buy the same products. I want a strong currency so that I get more for my money, not less. Notice how central bankers and politicians are on the same page? Weak currency causes price inflation: I demur.

Speaking of central banks: the European Central Bank and the US Federal Reserve both signaled that their next policy move could be an interest rate cut. They were not alone. The Reserve Bank of Australia hinted at the prospect of easing monetary policy even more after the quarter point cut earlier in the month; the Bank of Japan signaled readiness to ramp up stimulus as global risks cloud the economic outlook; and the Bank of England was slightly less hawkish amid mounting risks to the economy from a no-deal Brexit.

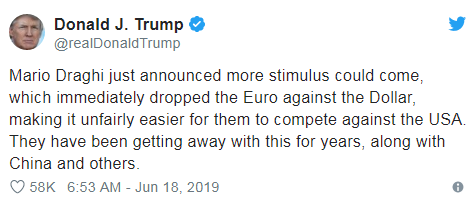

ECB President Mario Draghi kicked-off the second phase of the currency war at the institution’s annual forum on Tuesday in Portugal. He said that “additional stimulus will be required” if the economic outlook doesn’t improve. He added that the commitment to keeping interest rates low could be bolstered, further cuts remain “part of our tools,” and renewed asset purchases are an option even if that means raising self-imposed limits on how much it can buy. The euro fell on the comments.

This set off a tweetstorm from US President Donald Trump. We all know he has never hesitated to criticize the Fed Chairman Jerome Powell, so why should a foreign central banker be any different? It looks like we can add a currency war on top of his ongoing trade war

Look, Draghi isn’t stupid. He knew full well (just like the rest of us) that the day after he made that statement the Fed was poised to signal a rate cut. So, he made the prudent move in game theory: he used his words. He knew that the euro would tumble after his statement, but he also knew that when the Fed signaled rate cuts the next day, the euro would go up again.

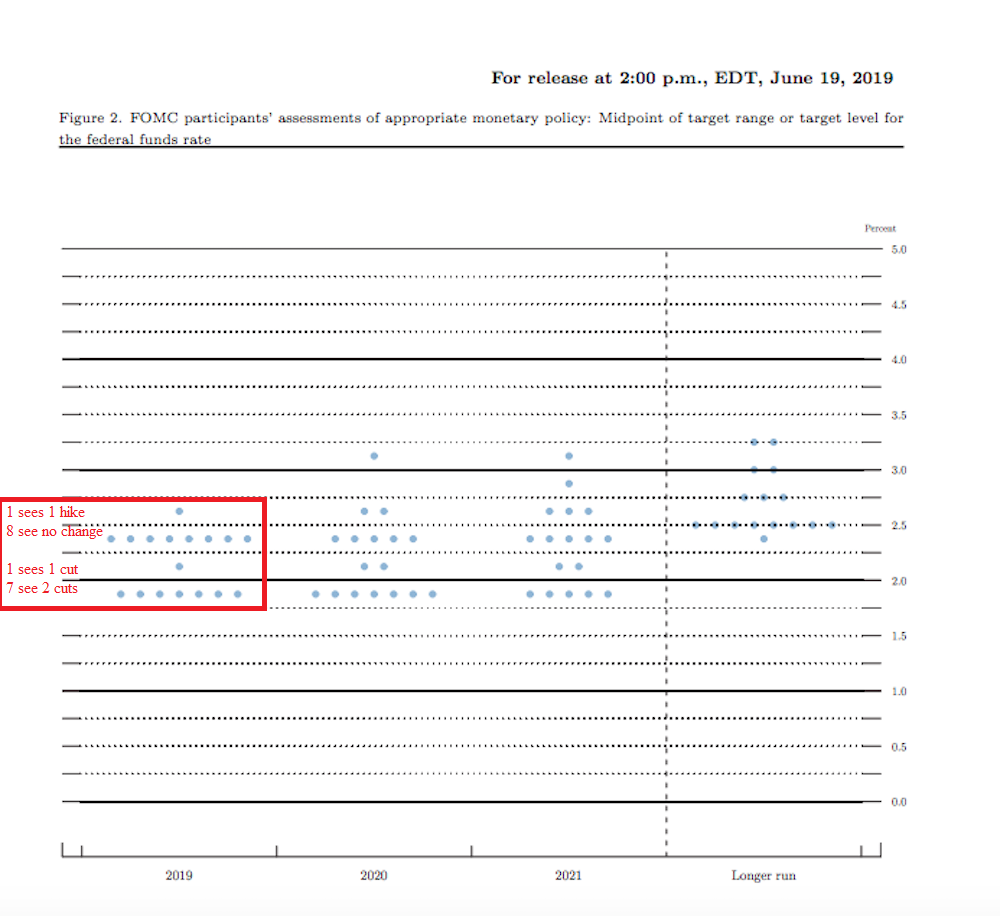

The next day, it was the Fed’s turn. Yada, yada, yada. I’ll spare you the details but suffice to say they gave the “all systems go” on the path to rate cuts. Interestingly, the Fed’s dot plot, which is a chart that records each Fed official's forecast for the central bank's key short-term interest rate, showed a house divided. Eight members saw no need to change rates this year, seven thought at least two cuts would be necessary, one thought that only one cut would be needed, and one member thought a hike would be appropriate. The decision to keep rates on hold wasn’t unanimous, however, with one member wanting a rate cut immediately. This was his first dissent since 2013 and the first by any committee member since 2017. With that, Mr. Market has fully priced-in a July quarter point cut, with a small chance of a half point cut, and the USD has responded in kind by falling against all the major currencies last week.

Bucking the worldwide trend of central banks looking at cutting rates, the central bank of Norway, Norges Bank, raised its key interest rate by a quarter point to 1.25% on Thursday and it indicated that there were more rate hikes in its pipeline. It was its third hike since last September. Norway is the largest oil and gas producer in Western Europe. The policy turn at the Fed will cause the USD to go down which in turn will cause the price of oil to rise. Higher energy prices will feed inflation, causing prices to rise for products and services that have an energy and/or transportation component to them. This in turn will justify future rate hikes to control inflation.

We can place Canada into the same position as Norway. Based on last week’s May inflation report, Canada has an inflation problem. Inflation rose faster than expected in May, jumping to 2.4% on the year across all eight major components. It was the highest annual rate since October, while core inflation (which is closely watched by policy makers) surged to the highest reading since February 2012. The rise in inflation supports the Bank of Canada’s view that “We the North” is emerging from its growth slowdown and Governor Stephen Poloz’s view that rates will need to go higher.

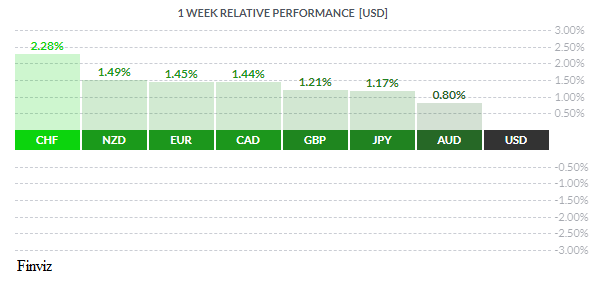

The CAD was on its way to being the top performer of the week until Friday’s retail sales report caused it to give back some of its gains, registering a gain of 1.44% on the week. Canadian retail sales came in a little less than expected at 0.1% instead of the 0.3% that was forecast. As I pointed out in Friday’s Reuters article, the data was an excuse to take profits on a pretty good run for the week. The CAD broke up and out of its downward trend after the solid jobs data from June 7th. As you can see from the chart below, it re-tested the breakout the following week and held the former resistance line which now becomes support. Year to date, the CAD is the strongest of the majors with a gain of 3.23%.

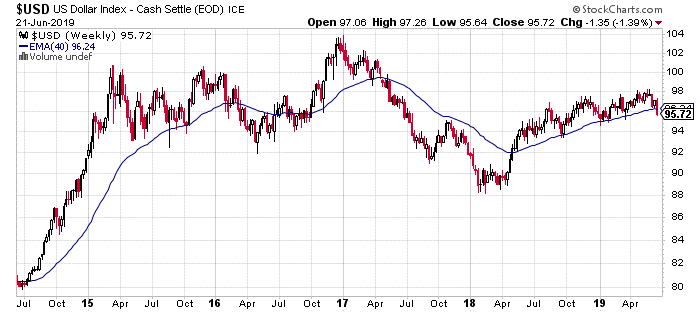

The US dollar index, a proxy of the USD trading against a basket of trading partners, has given up its 40-week moving average, which it has held for over a year. What does this mean? Well, if it were a stock, I would sell it.

Next week, the focus will turn to the G20 and the meeting between President Trump and Chinese Premier Xi.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, JUNE 24 | ||||

| TUESDAY, JUNE 25 | ||||

| All Day | All | OPEC Meetings | ||

| 10:00 | USD | CB Consumer Confidence | 132.0 | 134.1 |

| 13:00 | USD | Fed Chair Powell Speaks | ||

| 22:00 | NZD | Official Cash Rate | 1.50% | 1.50% |

| 22:00 | NZD | RBNZ Rate Statement | ||

| WEDNESDAY, JUNE 26 | ||||

| 05:15 | GBP | Inflation Report Hearings | ||

| 08:30 | USD | Core Durable Goods Orders m/m | 0.1% | 0.0% |

| 21:00 | NZD | ANZ Business Confidence | -32.0 | |

| THURSDAY, JUNE 27 | ||||

| 08:30 | USD | Final GDP q/q | 3.1% | 3.1% |

| Day 1 | All | G20 Meetings | ||

| FRIDAY, JUNE 28 | ||||

| 04:30 | GBP | Current Account | -32.0B | -23.7B |

| 08:30 | CAD | GDP m/m | 0.2% | 0.5 |

| 10:30 | CAD | BOC Business Outlook Survey | ||

| Day 2 | All | G20 Meetings | ||

|

Tony Valente Senior FX Dealer, Global Treasury Solutions |

|||