|

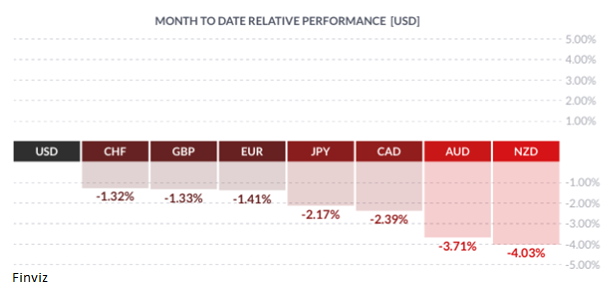

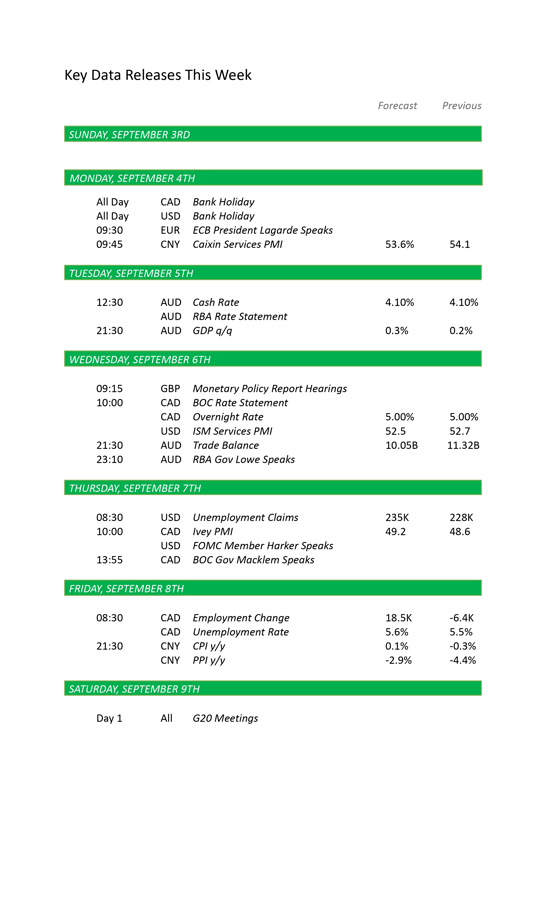

Higher for Longer to Just Longer King dollar has been on full display in August going up hard against all its competitors. The USD has actually been rallying since mid-July and it got the all-clear signal on July 26th after the Fed raised its target interest by 25 basis points to 5.25%-5.50%, resuming an aggressive rate-hiking campaign that began in March 2022 after temporarily pausing at the June meeting. The Fed also signaled that it could continue to raise rates at least one more time this year, since most officials view this as necessary to bring inflation down to the 2% target over time. Thus, judging by the relentless climb in the USD index, the market has clearly bought into the Fed’s higher-for-longer mantra, for now. I stress the “for now” comment because it appears that during the annual Jackson Hole gathering of global central banks from August 24 – 26 a shift in the monetary policy mindset has changed. Fed Chairman Jerome Powell gave a speech and two things stood out to me. Firstly, he never emphasized a desire to hold rates higher for longer. Secondly, he ended his speech by saying “we are prepared to raise rates further if appropriate, will proceed carefully”. Both insights tell me that he was no longer hawkish but rather marginally dovish. To me, he was basically saying that more rate hikes if necessary but not necessarily more rate hikes to come. Fed member Patrick Harker was more direct when asked about rate hikes – “Yeah so we clearly are going to hold through the end of the year, right. Next year, we just-- we need to let the data dictate that, right. We need to see what's going to happen.” In other words, monetary policy acts with a lag so they need to see how the rate hikes affect the entire economy. Remember, just because they stop hiking rates doesn’t mean that the current policy rate isn’t restrictive, it is still putting pressure on the economy. “Higher for Longer” wasn’t the only driver of the USD in August, growth divergence was just as important. Eurozone Q2 GDP is 0.3% and UK Q2 GDP is 0.2% compared to 2% for the USA. Currently, the Atlanta GDP growth rate is estimated to be 5.6% in Q3. This is all well and good, but cracks are starting to appear. The US flash Composite PMI data, which tracks manufacturing and service sectors, fell to a reading of 50.4 in August from 52 in July, the biggest drop since November 2022. While August's reading was the seventh straight month of growth, it was only fractionally above the 50-level separating expansion and contraction as demand weakened for both manufactured goods and services. Service sector business activity growth was the slowest since February at 51.0 in August, and the Manufacturing PMI fell deeper into contraction territory at 47.0 down from 49.0 in July, the fourth straight month of contraction. Remember, the PMI are surveys which measures purchasing manager’s mindset of the future, thus it will not be picked up by rear-view mirror indicators like GDP until after the fact. On the employment front, we had two reports that made the USD bulls think twice (black circle on USD Chart below) about pressing their luck. The JOLTS report is a monthly survey of job openings, hiring, and job separations (quits, layoffs, discharges) released by the BLS showed that the number of available jobs in the United States shrank for the third consecutive month, dropping below 9 million for the first time since March 2021. The jobs report released on Friday reinforces what we saw in the Jolts report. September nonfarm payrolls increased by 187,000 jobs last month after rising by 157,000 in July. Job growth averaged 150,000 per month over the past three months, sharply down from 238,000 in the three months through May. Also, the unemployment rate jumped to 3.8% and wage gains moderated, suggesting that labor market conditions were easing and cementing expectations that the Federal Reserve will not raise interest rates this month. The price action in the USD index over the last week is telling. The USD was unable to push past the June high after the recent flash PMI and employment reports, which has made the market less confident of a Fed rate hike later this month. In fact, market pricing on a Fed hike in September is down to 9.5%. There are two key events this month that may be less supportive of the USD. Firstly, the August CPI due on September 13 is most likely to show that inflation continues to come down. Secondly, political drama is brewing as the US is facing partial Federal government shutdown starting in early October because the two parties haven’t been able to agree on next year's spending. Drama and intrigue are not exclusive for the US, the ECB and the Bank of Canada have policy meetings this month which are difficult to gauge. The BOC is on tap this Wednesday. Canada's CPI rose to 3.3% in July (from 2.8% in June) and likely increased again in August which would be supportive of a rate hike. However, last Friday’s release of Q2 GDP showed that the domestic economy unexpectedly contracted at an annualized rate of 0.2%. The forecast was for a gain of 1.2%. I would think that this data will move the BOC to the sidelines as market chatter has gone from hikes to cuts. It would seem to me that the policy rate has reached its restrictive level. Even though the ECB policy rate is 3.75%, which is a lot less than other major countries (US 5.38%, UK 5.25%, Canada 5.00%) it already appears to be restrictive. The Eurozone economy is sputtering along without any growth at all. To make matters worse, the EU is about to reestablish its Stability and Growth Pact rules which were temporarily sidelined due to Covid and later the Russia war. The rules will curtail government budgets throughout Europe so fiscal support will not be there which will probably weigh on the euro.

|

|

by Tony Valente Senior FX Dealer, Global Treasury Solutions |

|||

Would you like to receive all of our blog posts directly to your inbox? Click here to subscribe!