Higher for Longer & No Landing

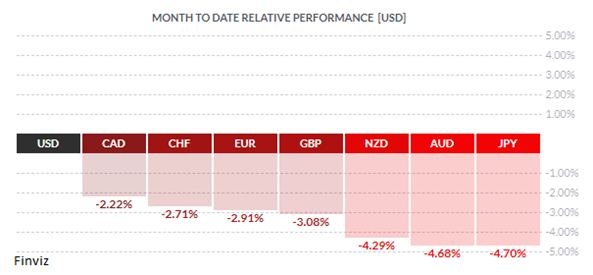

What a February it has been for the USD. It completely unwound all of its losses from January and added to its gains making it the best-performing currency against the other major currencies year to date. The USD was spurred higher by two dominant themes - #higherforlonger and #nolanding. These two themes emerged after the outstanding US January employment report, released on February 3rd, which showed that the American economy added 517,000 jobs in the month of January, and the unemployment rate ticked down to 3.4%, the lowest rate since May of 1969.

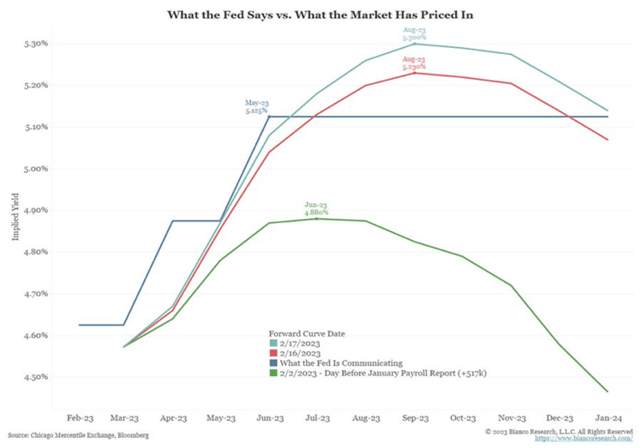

The jobs report kicked off a string of stronger-than-expected economic reports which caused the market to reprice the Fed’s interest rate hiking path, hence the higher for a longer theme. Prior to this month, all of the economic reports that were released in January painted a picture of a slowing economy and thus the market was anticipating the end of Fed rate hikes. Since the February 3rd jobs report, the market has priced in more tightening from the Fed. Then, there was virtually zero chance of the Fed hiking to 5.50% by June. Now, it’s nearly a 2/3 probability. The Fed Funds rate discounted for August is now 0.50% higher than it was on February 2. The rate cut that the market was pricing in for December 2023 was now pushed back to early 2024. For the first time in this rate hiking cycle, the market is pricing in more than the Fed is telegraphing.

For the economy, the string of strong economic reports released this month has caused market sentiment to swing from fear of a recession to optimism that one can be avoided, hence the no landing theme. This apparently means the global economy will bounce back with high employment, frustratingly persistent (but not lethal) inflation, and no recessionary outcomes. This rosy outcome will occur on the back of China’s reopening, the resilience of western economies, lower energy costs, plus rising post-Covid consumption patterns all combining to power the global economy through this uncertain patch.

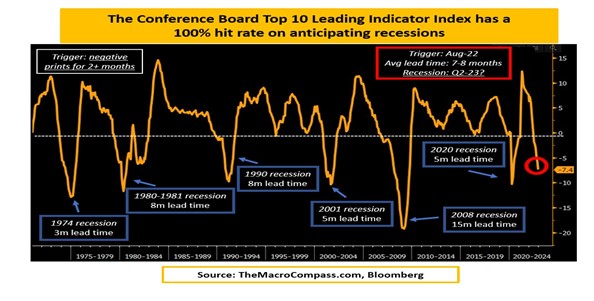

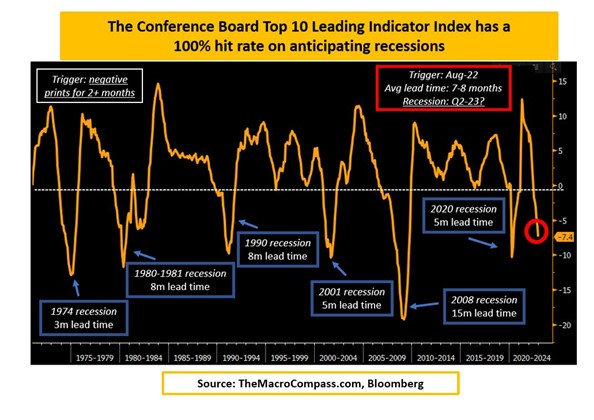

If you believe in this scenario, then you must believe in the tooth fairy. You would need to ignore the fact that all of the pertinent curve inversions are forecasting a recession and this time around they will be wrong. You would also need to suspend the belief that the 7.0% decline (annualized pace) of the index of leading economic indicators will not foretell a recession.

The reality is that the blockbuster employment report was a statistical anomaly, caused by unusually warm weather and methodological and seasonal adjustments by the Bureau of Labor Statistics following a very weak November and December. It will probably take another month of data to prove my point.

With this in mind, how much room does the USD have to run? In the chart below, the US dollar index looks like it will surpass last month, 2023 high thus far, and then try to extend to the 200-day moving average. The momentum indicators are still rising, are little stretched but have not begun to turn as of yet.

Since the euro represents 50% of the US dollar index we would expect the euro to continue on its downward path. All things considered, the euro is not in a bad spot, it seems to be gently consolidating lower while it waits for interest rate hikes by the ECB. The ECB will hike by 50 bps, lifting the deposit rate to 3.0%, on March 16th since ECB President Lagarde already pre-committed to a hike. The key will be what they telegraph next. The ECB hawks have been very boisterous about another 50 bps hike at their May 4th meeting. The euro may swing down to the 1.0450 level which is low for the year set back in January. I suspect the 200-day moving average should catch and support the currency as the no-landing theme unravels during the course of March.

In Canada, much was made of the Bank of Canada officially pausing its rate hiking cycle. Then, a couple of weeks later, Canada had a blockbuster employment report as well. The Canadian economy created 150k jobs in January. This caused the market to price in a 25% chance of a rate hike at the next meeting on March 8th, which would be an embarrassing turn of events for the BOC just 6 weeks after their pause. Luckily, subsequent reports for both the CPI and retail sales undershot expectations, helping the BOC save face.

As for the CAD, it is vulnerable to some more downsides for two reasons. First, the BOC is on hold while the other major central banks are still a couple of hikes away from an official pause. Secondly, the risk-off mode of the equity markets has hampered the CAD advance as the currency has been more correlated to the stock market than the price of oil. The CAD came within 20 pips of touching the 2023 high which was set in January on Friday. The next line of resistance is slightly over the 1.37 level, followed by the 1.38 level from early November. The slow stochastic indicator has curled and heading downward while the RSI and MACD are stretched. As I stated above, the major currencies should gently consolidate and turn as the no-landing and higher for longer themes unravels during the course of March.

|

by Tony Valente Senior FX Dealer, Global Treasury Solutions |

|||

Would you like to receive all of our blog posts directly to your inbox? Click here to subscribe!