Extra Innings

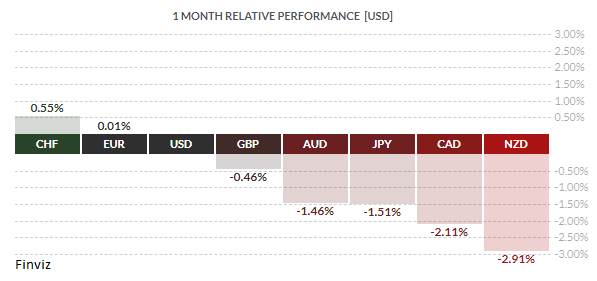

The Swiss franc was the top performer in October as market players rushed into the safe haven on the possibility that the current situation in Gaza could spiral into a greater conflict in the Middle East.

The USD has been a frontrunner since mid-July on the back of the “higher for longer” monetary stance by the US Federal Reserve. The combination of soaring yields and a more vigorous economy has underpinned the USD outperformance against its peers. However, with the Fed choosing to stand pat for the third consecutive FOMC meeting this past Wednesday, and some evidence of waning economic data, the tide in the USD looks to have turned.

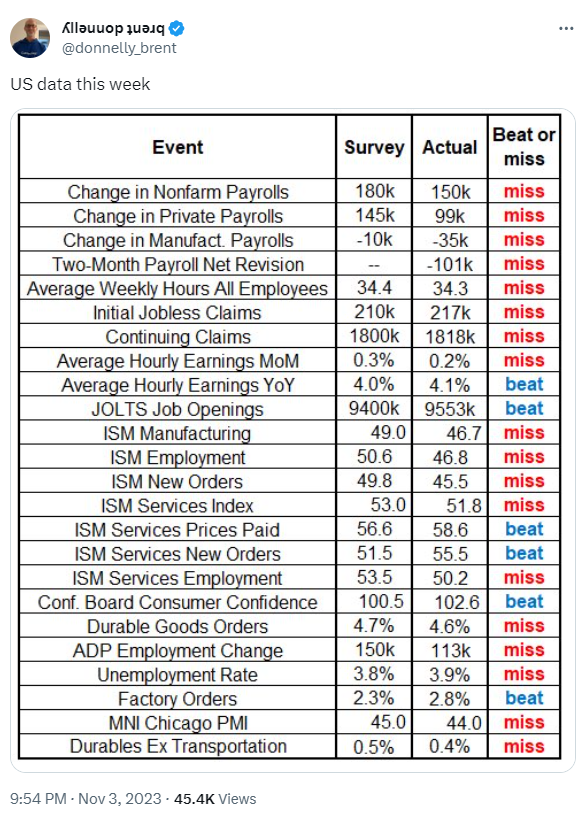

Let us start with the economic data. This past week we had way more misses then beats, which suggests that the economy may be softening. Also, the US economy just registered a GDP print of 4.9% growth for Q3. The most accurate forecaster has been the Atlanta Fed GDP Now indicator, which had Q3 at 5.0%. Well, it is now forecasting for Q4 only 1.2% growth as of November 1st (note, this doesn’t include Friday’s not so stellar jobs data), down from 2.3% on October 27th.

Now, lets have a look at Wednesday's Fed decision. As I mentioned earlier, they stood pat for third meeting in a row. During that time, yields were climbing due to a combination of the Fed’s higher for longer stance and the amount of Treasury issuance supply. Despite Fed Chairman Jerome Powell’s insistence that the Fed did not pause and confirmed that there is still no talk of a interest rate cut, the market decided otherwise. Prior to Wednesday's meeting the Fed funds futures market was pricing in 74 bps of cuts by the end of 2024. That's up to 99 bps now, so a full cut has been priced in. Also, the timing of cuts has moved up. The market now sees an 80% chance of a cut in May with 50 bps of cuts priced in by the July 31 FOMC meeting.

So, there you have it, the market is convinced that that softness in the economy, which is what the Fed wanted to see to combat inflation, is now here. And this is the reason why the USD has sold off this week.

The US dollar index, which is a proxy of the USD against its trading partners, posted a bearish outside down on the weekly chart, trading on both sides of the previous week's range and settling below the prior week’s low. The momentum indicators on the daily chart below are all waning and the SAR indicator just printed its first downward dot (at 106.99) in 8 trading days. Also, the 5-day moving average crossed down through the 20-day moving average for the first time since late July. The index’s next target is initial the 104.40 area followed by 103.45, which is around where the 200-day moving average can be found.

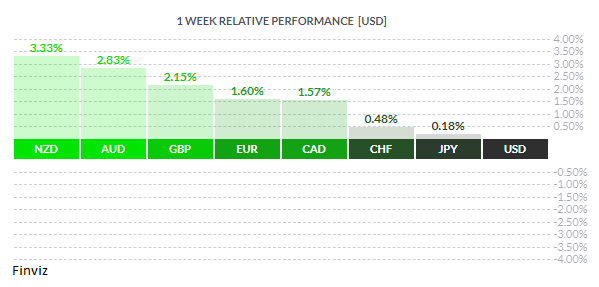

Meanwhile, the euro, which makes up a little more than 50% on the US dollar index, posted a bullish outside up week, which makes sense since the US dollar index posted a bearish outside on the weekly. The momentum indicators are all flashing the “all clear” sign. Like the dollar index above, the 5-day moving average for the euro also crossed the 20-day, the first time since last October. The euro’s next target is initial the 1.0760 area followed by 1.0860, which is around where the 200-day moving average is now.

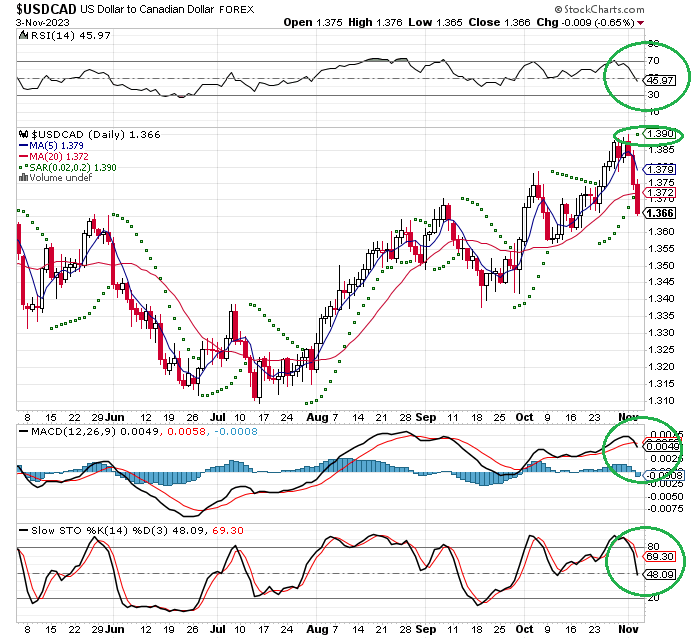

It is the same story for the GBP and the CAD. The momentum indicators are all conducive to more gains. The 5-day moving average crossed the 20-day and the next targets are near their 200-day moving average, 1.2430 for the GBP and 1.3490 for the CAD.

It is important to point out here that the move in these currencies is not related to their fundamental prospects but rather the backdrop around their USD counterpart. In fact, the Eurozone economy has been basically flat all year, the UK economy has been in a contraction since July, and the Canadian economy may already be in a recession since the sum of its monthly GDP prints from February through August (6 months) has been zero.

The Yen is the only outlier, mostly because it is the only central bank with a negative policy rate. The Bank of Japan held its monetary meeting the day before the Fed did and the market was disappointed that in didn’t act more forcefully. They downgraded the importance of the 1.0% ceiling of the 10-year bond yield control by now calling it the reference rate. It was a baby step

forward by de-emphasizing its importance in order to lay the groundwork for an eventual move out of negative interest rates. Of course, with it being the only bank with negative rates it has a target on its back for speculators, thus one must be wary of possible BOJ intervention in the currency market as it defends the 150 level.