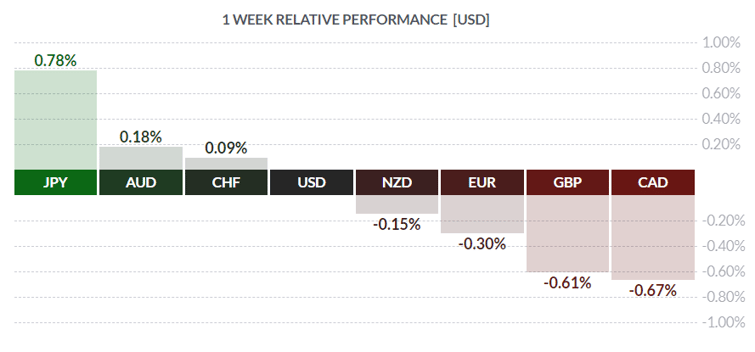

Courtesy FinViz

It has appeared, at least for a while, that the ongoing trade ‘spat’ between the Americans and the Chinese would remain confined to those two trading giants, while others such as Mexico, Canada, and the European Union would escape attention. While it is true that President Trump recently took aim at European auto exports to America, still the view was that the US-China trade discord would remain front and center. Well, apparently not. There were also interesting developments in the bond market and the oil market, so let’s look at what happened last week.

To begin with, the week saw some interesting statistics released in North America. Canada’s +0.5% GDP in March beat the call of +0.3% and bested the previous month’s decline of -0.1%. The entire quarter registered growth of +0.4%, which lagged the call of +0.7%. Still, it seems that growth perked up markedly at the end of Q1 with perhaps a strong hand-off to Q2.

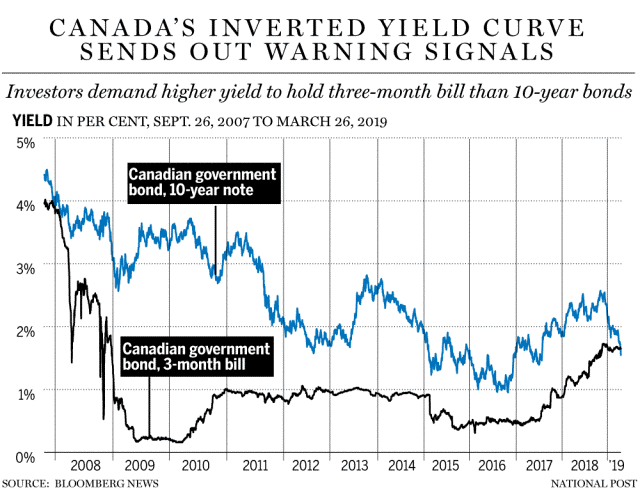

On Wednesday, Bank of Canada governor Stephen Poloz left Canada’s overnight rates unchanged while providing an upbeat assessment of the economy. He claimed that the economy had been in a ‘soft patch’ at the start of the year but that growth appeared to be resuming. The governor also tried to get the message across (as discreetly as possible) that the Bank’s next move would be to raise rates. On that, he has shown himself to be an optimist along with Fed boss Jay Powell, and quite unlike his gloomy colleagues elsewhere. Mr. Market was evidently unimpressed as the loonie failed to rally in any meaningful sense, perhaps because inter alia bond markets globally are rallying sharply, and that is never a good sign. We have noticed a marked decline in bond yields in recent weeks so, seeking enlightenment, we spoke with our friend the bond salesman.

Simply put, the salesman said, the Canadian and American bond yield curves are inverted. That’s a technical way of saying that it costs more to borrow short-term than long-term and is invariably a sign of looming economic recession. The chart below shows how the Canada 10-year yield dropped below the three-month treasury bill yield in recent weeks.

The American yield curve, from overnight to 30 years, is an even more dramatic illustration of inversion. With the recent rally in yields following President Trump’s imposition of new tariffs on Mexican goods, this curve will be even more inverted.

So, what does all this mean? The bond salesman replied that, while politicians talk up the economy and central bankers in North America imply a bias to future tightening, the bond market (that mass of jumpy fraidy-cats) simply doesn’t believe them.

The USD started last Friday on a strong note following Trump’s Mexican tariff bombshell but faded to close out the week. However, with growth faltering elsewhere in places like Germany, it is becoming hard to maintain optimism on the global growth outlook.

German jobless numbers rose +60K vs the call of -8K, with the rate rising to 5.0% from 4.9%. This is coming after a slowdown in industrial production mentioned in recent articles and does not augur well for the Eurozone where interest rates are already in negative territory. Not good news for the Euro and yet more negative news for the ECB to contend with.

With his imposition of a new 5% tariff on Mexican imported goods, and the possibility of further future hikes (ostensibly to resolve the illegal immigrant issue), US president Trump has ratcheted up the stakes in the ongoing global trade spat. (We hesitate to use the term ‘trade war’ as we don’t think it has yet reached that stage). Predictably, markets reacted negatively. Players ignored the downward revision in US Q1 GDP from 3.2% to 3.1% and piled into US treasury bonds and the greenback, awaiting further clarity on this tariff issue. As we have pointed out before, a rising USD generally means falling commodity prices, and last week was no exception as WTI crude plunged to the $53.50 USD/bbl from the mid-60 range seen early last week. American crude production continued near record highs despite falling prices and fears of a slowing global economy. It should go without saying declining crude prices are not good for the loonie.

The coming week sees the all-important employment statistics in both Canada and the US, along with an avalanche of fedspeak.

Key Data Releases This Week

| Forecast | Previous | |||

| MONDAY, JUNE 3 | ||||

| 10:00 | USD | ISM Manufacturing PMI | 53.0 | 52.8 |

| 21:30 | AUD | Retail Sales m/m | 0.2% | 0.3% |

| TUESDAY, JUNE 4 | ||||

| 00:30 | AUD | Cash Rate | 1.25% | 1.50% |

| 00:30 | AUD | RBA Rate Statement | ||

| 05:30 | AUD | RBA Gov Lowe Speaks | ||

| 09:55 | USD | Fed Chair Powell Speaks | ||

| 21:30 | AUD | GDP q/q | 0.4% | 0.2% |

| WEDNESDAY, JUNE 5 | ||||

| 10:00 | USD | ISM Non-Manufacturing PMI | 55.6 | 55.5 |

| THURSDAY, JUNE 6 | ||||

| 04:25 | JPY | BOJ Gov Kuroda Speaks | ||

| 05:00 | GBP | BOE Gov Carney Speaks | ||

| 07:45 | EUR | Monetary Policy Statement | ||

| 08:30 | CAD | Trade Balance | -3.2B | |

| 08:30 | EUR | ECB Press Confernece | ||

| FRIDAY, JUNE 7 | ||||

| 08:30 | CAD | Employment Change | 106.5K | |

| 08:30 | CAD | Unemployment Rate | 5.7K | |

| 08:30 | USD | Average Hourly Earnings m/m | 0.3% | 0.2% |

| 08:30 | USD | Non-Farm Employment Change | 180K | 263K |

| 08:30 | USD | Unemployment Rate | 3.6% | 3.6% |

|

by DAVID B. GRANNER Senior FX Dealer, Global Treasury Solutions |

|||