Courtesy of FinViz

In light of strong US employment numbers released last Friday, and what appears to be mixed signals elsewhere in the global economy, the railway train metaphor seems apt. Let’s take a closer look, starting with the True North.

As was widely expected, last Wednesday the Bank of Canada maintained its overnight rate at 1.75% - the ninth straight meeting without a change. However, market players – who had been anticipating a rate cut by the Bank early next year – saw their hopes dashed by a surprisingly upbeat assessment of current economic trends in the Bank’s accompanying statement. Our learned colleagues Dr. Long and Mr. Short parsed the release for these salient points:

- Nascent evidence the global economy is stabilising

- Global growth looks set to edge higher in next few years, although trade disputes present a risk

- Q3 growth in Canada slowed, as predicted, to 1.3%

- Domestic capex unexpectedly strong in transportation and engineering

- Domestic inflation still around the Bank's target of 2%

Investors took this as a somewhat hawkish statement, one apparently ruling out any near-term cuts in administered rates and bought the loonie with a vengeance knocking it out of its current trading range.

That was Wednesday. Last Friday saw the release of what can fairly be described as disastrous Canadian November jobless numbers. They were not pretty.

Analysts had called for a loss of -9K jobs with the jobless rate holding steady at 5.5%. In actuality, the numbers emerged at a loss of -71.2K jobs (FT -38.4 // PT -32.8), with the rate jumping to 5.9%. The loss in part-time jobs is surprising given that, at this time of year, retailers are usually hiring seasonal help for the Christmas shopping season. What does this imply for the all-important holiday season for retailers? There really is no good way to spin these numbers, although federal politicians will make the attempt.

The upshot is that Canadian rate cuts are once again on the agenda, and the loonie dropped 3/4s of a cent as a result, giving up ground gained earlier in the week.

In the Eurozone, talk had been that the zone had turned the corner on growth. Or, in other words, it was believed that Germany had turned the corner on growth, narrowly avoiding recession and preparing to pull the rest of the zone out of its current funk. With interest rates below zero and the ECB making clear it would cut rates even further into negative territory if necessary, the zone took on a patina of strength. Which is all it was.

German Industrial Production virtually collapsed in October, declining -1.7% vs the call of +0.1%. Auto production was the chief culprit, falling a precipitous 5.4% mth/mth. All of this sent Industrial Production down 5.3% yr/yr – the biggest drop in ten years.

Courtesy Bloomberg

'Das ist nicht gut'

With paymaster Germany limping along, the EUR was one of the weaker currencies on the week, hit by a resurgent greenback.

However, earlier in the week, the greenback had been laid low by several factors. Chinese PMI indices had risen above the crucial 50.0 level, while the widely watched US ISM number for November disappointed at 48.1, below the call of 49.4 and falling from the previous month’s 48.3. The ADP employment index released last Wednesday came in at +67K jobs, well below the call of +140K jobs and causing traders to revise downward their bets on last Friday’s employment numbers. Additionally, the ever-mercurial President Donald Trump made several disparaging remarks early in the week about the ongoing Sino-US trade talks, even saying that he might wait until after the 2020 election to ink a deal (!). Clearly, market players don’t like this sort of talk and the greenback suffered as a result.

Weakness in the ISM non-manufacturing index (53.9 vs call 54.5, last 54.7) led analysts to think that, maybe, the recession long-predicted and eagerly anticipated by the bond market might finally be materialising. This also led to the view that the global economy might be stabilising at a lower level of growth.

That was the first four days of last week. Then Friday rolled along and blew everything away – a sluggish USD, timid jobs forecasts, a booming bond rally, equity indices trading lower on a daily basis – all the usual negative stuff.

Following the dismal ADP report, analysts wrote that the call for November jobs at +185K was too high, and the actual number would be much lower. It turns out that these analysts, and just about all market players, were dead wrong. The US economy added an astonishing +266K jobs, with the rate declining to 3.5% from the prior 3.6%. The two-month net revision was a strong +41K jobs. Striking GM workers returning to work helped manufacturing jobs rise by 54K – the strongest in 21 years!

As if to spook the bond market further, the December read of Consumer Confidence from the University of Michigan rose to 99.2 from the previous 96.8 and dusting the call of 97.0 from analysts.

Mr. Market was quite impressed and bought the greenback. Although the USD was the loser on the week, still it had developed some momentum going into today. The engine evidently still has a good head of steam! This train – with America in the lead and other economies following behind – should now be rolling along nicely.

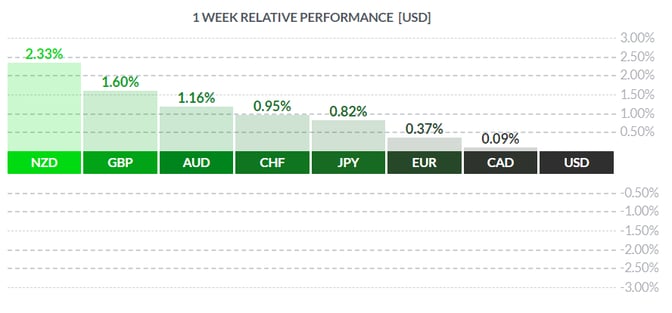

Next Thursday sees the crucial British election, and some analysts are calling it ‘Boris Johnson’s to lose’. Sterling rallied sharply on the positive sentiment, picking up ground against the USD to its best level in seven months.

The resolution of this tiresome Brexit issue, which appears likely although it is not yet done, will be a major boost to the global economy and will free the UK to seek new trade relationships. Should trade talks between the US and China finally produce an agreement, two major points of contention will be removed, and the overall global economic outlook should improve markedly.

The coming week sees the aforementioned UK election, little in the way of statistics from Canada, and a slew of secondary numbers from America, as well as a Federal Reserve rate announcement and a press conference with Fed boss Jay Powell on Wednesday afternoon.

Key Data Releases This Week

|

by DAVID B. GRANNER Senior FX Dealer, Global Treasury Solutions |

|||